SMM June 18 News:

Metal Market:

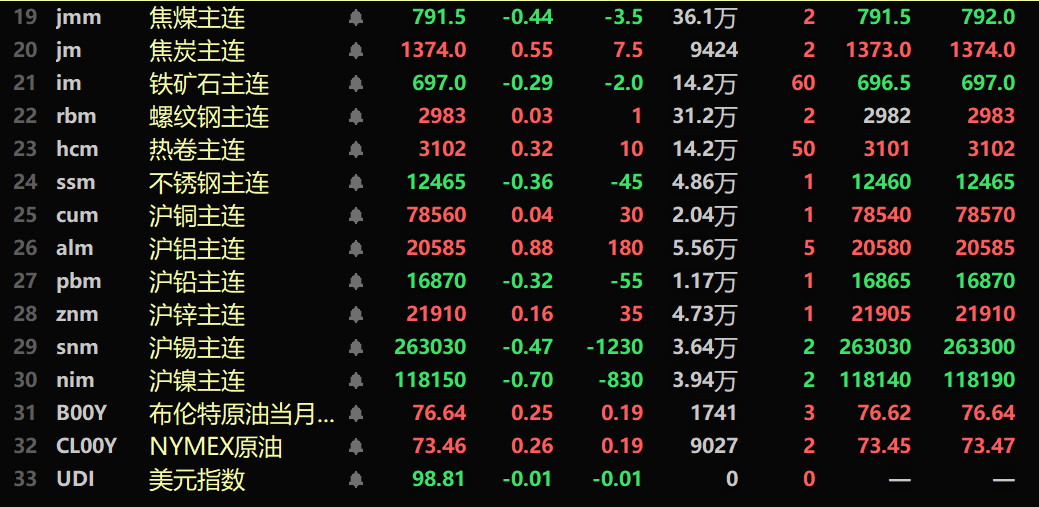

Overnight, domestic market base metals showed mixed performance, with SHFE tin falling 0.47%, SHFE copper rising 0.04%, SHFE nickel dropping 0.7%, SHFE lead decreasing 0.32%, SHFE aluminum increasing 0.88%, and SHFE zinc rising 0.16%. In addition, the most-traded alumina futures rose 1.47%, and the most-traded continuous casting aluminum futures increased 0.38%.

Overnight, the ferrous metals series showed mixed performance, with iron ore falling 0.29%, stainless steel decreasing 0.36%, rebar slightly rising, and HRC increasing 0.32%. In terms of coking coal and coke: coking coal fell 0.44%, and coke rose 0.55%.

Overnight, overseas market metals generally declined, with LME copper falling 0.34%, LME aluminum rising 1.25%, LME lead dropping 1.57%, LME zinc decreasing 0.81%, LME tin falling 1.13%, and LME nickel dropping 0.89%.

Overnight, precious metals: COMEX gold fell 0.32%, while COMEX silver rose 2.01%. Overnight, SHFE gold rose 0.04%, and SHFE silver increased 1.71%.

The World Gold Council released the "Central Bank Gold Reserves Survey 2025" (CBGR) on the 17th. The survey collected responses from 73 central banks worldwide. Nearly 43% of central banks plan to increase their gold reserves in the coming year. The World Gold Council believes that, despite gold prices repeatedly hitting new highs and global central banks having net purchased gold for 15 consecutive years, central banks still favour gold. Data shows that over 90% (95%) of the surveyed central banks believe that global central banks will continue to increase their gold holdings in the next 12 months. This proportion marks the highest since the survey was first conducted on this issue in 2019 and also represents a 17 percentage point increase from the 2024 survey results. The survey points out that economic and geopolitical uncertainties persist and impact central banks' strategies, so gold will continue to serve as a safe-haven asset to hedge against these risks.

Citi said in a report that silver prices could rise to $40 in the next 6 to 12 months. The bank added, "We expect that consecutive years of deficits, sticky shareholders demanding higher prices to sell, and robust investment demand will tighten silver supply." In an optimistic scenario, silver prices could reach $46 per ounce by Q3 2025, boosted by a faster resolution of trade tensions and a hawkish US Fed policy.

As of 8:12 on June 18, overnight closing prices

》Click to view SMM Futures Data Dashboard

Macro Front

Domestic:

[SAFE: Foreign Investment in Domestic Stocks Further Increased in May MoM] Li Bin, Deputy Director of the State Administration of Foreign Exchange (SAFE) and spokesperson, stated that in May, the overall supply and demand of foreign exchange in China were balanced, and the foreign exchange market operated smoothly. First, cross-border capital flows continued to record net inflows. In May, non-bank sectors, including enterprises and individuals, saw a net inflow of US$33 billion in cross-border capital. Among them, the net inflow of capital from trade in goods remained at a relatively high level. Foreign investors further increased their holdings of domestic stocks compared to the previous month. The net outflow of capital from services trade, dividend and interest payments by foreign-invested enterprises, and outward direct investment remained generally stable. Second, market expectations remained stable. In May, banks' foreign exchange settlement and sales turned to a surplus. Enterprises and individuals maintained a stable willingness to settle foreign exchange, while the demand for foreign exchange purchases pulled back, resulting in rational and orderly market transactions. Currently, China's economy is maintaining an overall stable development trend with steady progress, which will continue to provide strong support for the stable operation of the foreign exchange market. 》Click to view details

》The 2025 Lujiazui Forum opened on June 18 (with the latest agenda attached)

[Coal inventory at main ports in the Bohai Rim region stood at 28.68 million mt, down 13.5% from the previous peak]According to data from the National Bureau of Statistics (NBS), coal production from January to May totaled 1.9854 billion mt, with a YoY growth rate of 6.0%, a decrease of 0.6 percentage points compared to the growth rate from January to April. June is Safety Production Month, coupled with stricter environmental protection inspections in major production areas and pressure on sales, there are signs of further contraction in production. CCTD monitoring data shows that as of mid-June, the capacity utilization rate of sample coal mines in Shanxi, Shaanxi, and Inner Mongolia was 80.7%, lower than the average level in May and 1.5 percentage points lower than the same period last year. In terms of ports, although market prices have remained relatively stable, it is still difficult for sellers to actually ship goods. Coupled with the impact of inverted shipping costs, the volume of spot cargo arriving at ports has continued to be suppressed, and port inventory has maintained a downward trend. According to CCTD monitoring, coal inventory at main ports in the Bohai Rim region currently stands at 28.68 million mt, a decrease of 4.48 million mt from the previous peak, representing a decline of 13.5%.

US dollar:

The US dollar index rose 0.68% overnight, closing at 98.82. Softening US economic data and geopolitical tensions in the Middle East have made the market nervous. US retail sales in May were weaker than expected, but consumer spending remained supported by robust wage growth. The US dollar initially weakened after the data release, but quickly reversed its decline as the market digested the mixed signals reflected in the data. The US Fed is expected to announce its policy decision on Wednesday, followed by a press conference by Chairman Powell. The market generally expects the Fed to maintain its target range for the benchmark overnight interest rate at 4.25%-4.50%, where it has remained since December last year. However, the focus will still be on any guidance regarding the interest rate outlook.

Other currencies:

The market is closely watching the decisions of other central banks, including those of the Bank of England and the Riksbank later this week, to gauge future market trends. (Webstock Inc.)

Data:

Today, the UK's May CPI year-on-year rate, UK's May core CPI year-on-year rate, UK's May retail price index year-on-year rate, Eurozone's May harmonized CPI year-on-year rate - unadjusted final value, Eurozone's May core harmonized CPI year-on-year rate - unadjusted final value, US's May preliminary monthly rate of building permits, US's May preliminary annualized total of building permits, US's initial jobless claims for the week ending June 14, US's continuing jobless claims for the week ending June 7, US's May monthly rate of housing starts (annualized), and US's May annualized total of housing starts, among other data, will be released. Additionally, notable events include: the Bank of Canada releasing the minutes of its monetary policy meeting; Bank of Canada Governor Macklem delivering a speech on Canada's economic outlook, inflation trends, and interest rates; and the 2025 Lujiazui Forum being held in Shanghai.

Crude Oil:

Both oil futures rose sharply, with US oil up 4.97% and Brent oil up 5.41%. The ongoing conflict between Iran and Israel, with no end in sight, has sparked concerns about supply disruptions, supporting oil prices, despite the fact that major oil and natural gas infrastructure and trade have so far not been substantially affected.

Data released by the American Petroleum Institute (API) on Tuesday showed that US crude oil and gasoline inventories fell last week, while distillate inventories rose. As of the week ending June 13, crude oil inventories decreased by 10.1 million barrels. Gasoline inventories decreased by 202,000 barrels, while distillate inventories increased by 318,000 barrels. Analysts had previously expected crude oil inventories to fall by about 1.8 million barrels, distillate inventories to increase by about 400,000 barrels, and gasoline inventories to increase by about 600,000 barrels last week. The market is now focusing on the weekly crude oil inventory report from the US Energy Information Administration (EIA), which will be released on Wednesday.

Despite the possibility of supply disruptions, there are signs that oil supply remains sufficient amid expectations of declining demand. In its monthly oil report on Tuesday, the International Energy Agency (IEA) lowered its forecast for world oil demand by 20,000 barrels per day from last month's projection and raised its supply forecast by 200,000 barrels per day to 1.8 million barrels per day. (Webstock Inc.)